Few decisions shape a Dubai property purchase more than the choice between an apartment and a villa. It is not simply a question of size or budget — the two asset types behave differently as investments, attract different tenants, carry different running costs, and reward different kinds of owner. An investor chasing monthly cash flow and a family looking for a forever home will, quite reasonably, land on opposite answers.

This guide walks through the real trade-offs so you can decide with clear eyes rather than on impulse. The only live market figures we cite come from the latest DLD and market data.

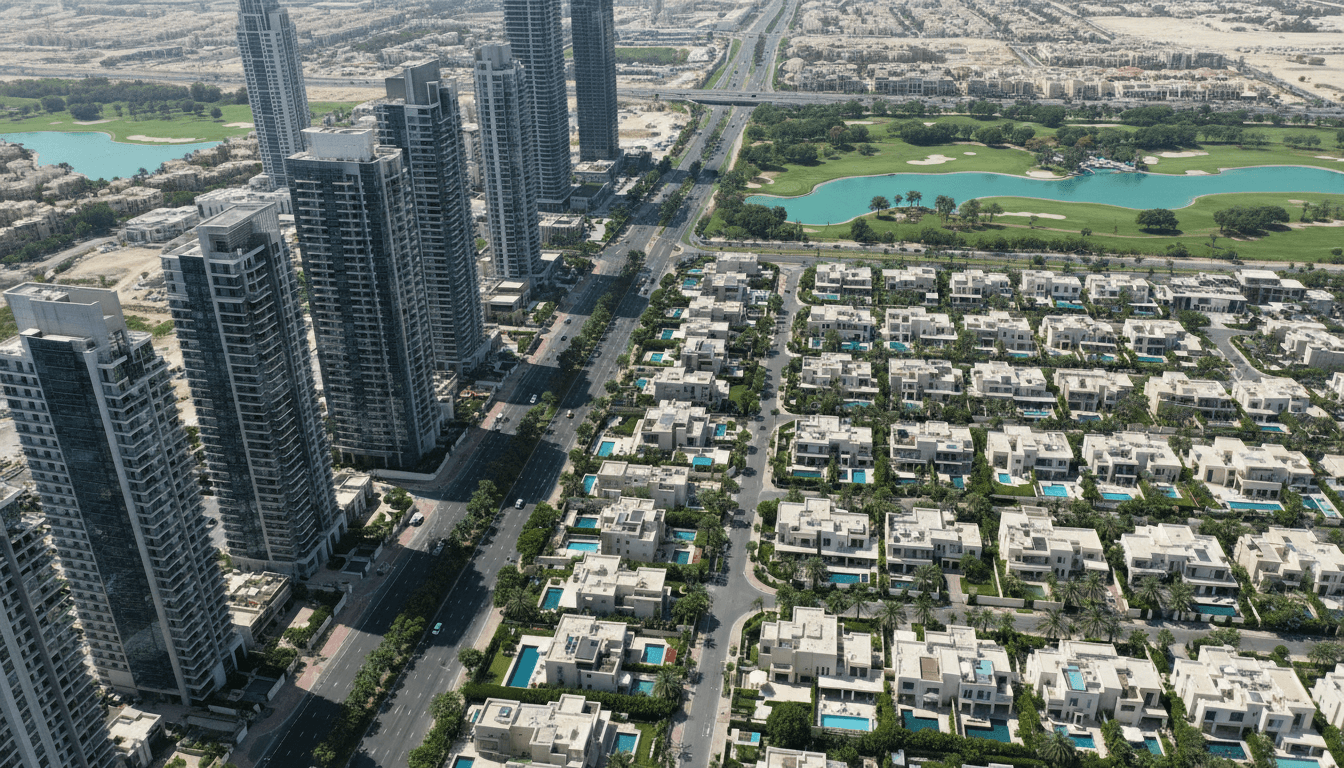

The core difference

At the simplest level, an apartment is a unit within a shared, multi-storey building, while a villa (or townhouse) is a low-rise home, usually with its own plot, garden, and often private parking. But the practical differences run deeper than the walls.

- Apartments concentrate people and amenities vertically. You share the land, the lobby, the pool, the gym, and the structure with dozens or hundreds of other owners. Density is high, and so is convenience.

- Villas spread out horizontally. You typically own or have exclusive use of the plot, control your own outdoor space, and have far more privacy — but you also shoulder more of the upkeep yourself.

Dubai offers both in abundance across designated freehold areas, where foreigners are free to own outright. Well-known apartment districts include Downtown Dubai, Dubai Marina, Jumeirah Village Circle, and Business Bay; established villa and townhouse communities include Arabian Ranches, The Springs, Dubai Hills Estate, and Tilal Al Ghaf. Always verify current pricing for a specific unit rather than assuming a community-wide figure.

Entry price and financing

Apartments are the more accessible entry point. Studios and one-bedroom units sit at the bottom of the market, which is why they dominate first-time-buyer and investor activity. Villas, needing land plus a larger built-up area, start considerably higher and rise steeply with plot size and location.

The financing rules are identical in structure for both. Under UAE Central Bank caps, residents can borrow up to 80% loan-to-value on a first property, while non-residents are limited to around 50%; off-plan and higher-value purchases attract lower caps. Because a villa's absolute price is higher, the same LTV percentage translates into a much larger cash deposit. A buyer who can comfortably fund a 20% deposit on an apartment may find the equivalent deposit on a villa out of reach, even though the loan mechanics are the same.

Transaction costs scale with price and apply equally to both types:

- DLD transfer fee: 4% of the purchase price.

- Agency commission: around 2% (plus 5% VAT).

- Ejari tenancy registration (if you later rent it out): around AED 220.

Worked example (hypothetical, for illustration only): On a property priced at AED 1,500,000, the DLD transfer fee would be AED 60,000 and agency commission roughly AED 30,000 before VAT. Double the price for a villa and those same percentages double in cash terms. The rates never change — but the cheque does.

Off-plan purchases (about 72% of the current market, roughly 65,300 off-plan versus 25,400 secondary listings) are registered via an Oqood with the DLD and protected by developer escrow accounts, while a ready home comes with a title deed. This applies to both types, though off-plan villa communities often sell in phased releases that stretch payment over construction.

Rental yield: apartments vs villas

This is where the two diverge most sharply as investments. The citywide average gross rental yield sits at around 4.7%, but that headline masks a consistent pattern: apartments tend to produce higher gross yields, while villas tend to reward capital growth and end-user demand.

The logic is straightforward. Apartments cost less to buy but command rents that are high relative to their price, especially compact studios and one-bedroom units in high-footfall areas. That compresses the price-to-rent ratio and lifts the yield. Villas cost far more per unit, and while their rents are also higher in absolute terms, rent rarely rises as fast as the purchase price — so the yield percentage is usually lower.

That does not make villas worse investments. It makes them a different investment:

- Apartments lean towards income. If your priority is monthly cash flow and a faster nominal return on capital, apartments generally do the heavier lifting.

- Villas lean towards appreciation. Limited land supply, strong owner-occupier demand, and the lifestyle premium of private space have historically supported robust capital growth, which shows up as equity gain rather than rental income.

Crucially, the UAE levies no income tax on rental income, no capital-gains tax, and no annual property tax — so whichever way your return arrives, cash flow or appreciation, you keep the headline figure and simply net off your own costs.

Service charges and maintenance responsibilities

Running costs are one of the most misunderstood parts of the decision, and they split the two types cleanly.

Apartments carry service charges levied by the building's owners association, calculated per square foot and covering shared facilities: the lobby, lifts, pool, gym, security, and structural maintenance. You pay these whether or not you use the amenities, and in amenity-rich towers they can be significant. The upside is that almost everything outside your front door is handled for you — you are buying convenience.

Villas usually carry lower community service charges per square foot because there are fewer shared facilities to fund. But that saving is partly illusory: as a villa owner you are directly responsible for your own home and plot. Garden upkeep, the private pool, exterior painting, plumbing, air-conditioning servicing, and eventual roof or structural repairs all fall to you. Budget for them, because they do not disappear — they simply move from a monthly community bill onto your own shoulders.

A useful way to frame it: with an apartment you outsource maintenance and pay for it predictably; with a villa you insource it and pay for it variably.

Lifestyle and tenant profiles

The two asset types attract distinctly different residents, which matters enormously if you are buying to let.

- Apartments suit singles, couples, young professionals, and investors' short- and medium-term tenants. They cluster around metro lines, business districts, dining, and nightlife. Tenants prize location, amenities, and a lock-and-leave lifestyle, and they tend to turn over more frequently.

- Villas suit families and long-term end-users. Tenants want schools nearby, gardens for children, space for pets, community parks, and quiet. They typically sign longer leases and stay put, which means lower vacancy churn and more stable, if lower-yielding, income.

If you value tenant stability and a low-hassle, long-hold profile, villas often deliver it. If you want a liquid, easily re-let unit in a deep pool of demand, apartments generally win.

Liquidity and resale

Liquidity — how quickly and easily you can sell — favours apartments. With around 90,700 residential transactions recorded so far in 2026 (year to date, roughly six months), the market is active, but that activity is not evenly distributed. Apartments trade in far greater volume, at lower price points, to a broader base of both investors and end-users. That depth means a well-priced apartment usually finds a buyer faster.

Villas sit in a shallower, higher-value pool. When demand is strong they can sell quickly and at a premium, but the buyer base is smaller and more selective, and in a softer market a villa can take longer to move. The trade-off is that scarcity also protects villa values on the way up.

Capital-growth patterns

Over full market cycles, villas have tended to show stronger and steadier capital appreciation, underpinned by finite land and persistent owner-occupier demand. Families buying to live — not to flip — are less price-sensitive and less likely to sell in a downturn, which supports values.

Apartments can appreciate strongly too, particularly in prime, supply-constrained locations, but the sector is more exposed to new-build supply. A wave of off-plan handovers in a district can cap short-term price and rent growth for existing units. This is why apartment investors watch the pipeline closely, while villa investors watch land availability.

Neither pattern is a guarantee, and Golden Visa eligibility applies to both: property from AED 2 million meets the 10-year renewable residency threshold, with a residence-visa route available from AED 750,000. For many international buyers, that residency benefit sits alongside the pure investment maths.

Who each one suits

An apartment is usually the better fit if you:

- Want the highest gross rental yield and monthly cash flow.

- Have a smaller deposit and want a lower absolute entry price.

- Prioritise liquidity and the ability to sell or re-let quickly.

- Prefer predictable, outsourced maintenance.

- Are targeting professional or transient tenants near business and transport hubs.

A villa is usually the better fit if you:

- Are buying as a family end-user, or targeting long-lease family tenants.

- Prioritise capital growth and equity over monthly income.

- Have the deposit and cash reserves for a higher-value purchase and hands-on upkeep.

- Value privacy, outdoor space, and community living.

- Are comfortable with a longer hold and slightly lower liquidity.

Side-by-side comparison

| Factor | Apartment | Villa |

|---|---|---|

| Typical entry price | Lower, broad range from studios up | Higher, driven by land and built-up area |

| Deposit needed | Smaller in cash terms | Larger in cash terms |

| Gross rental yield | Generally higher | Generally lower |

| Capital growth | Solid in prime areas, supply-sensitive | Historically stronger and steadier |

| Service charges | Higher per sq ft, covers shared amenities | Lower per sq ft, but you fund own upkeep |

| Maintenance | Mostly outsourced to owners association | Largely your own responsibility |

| Typical tenant | Singles, couples, professionals | Families, long-term end-users |

| Liquidity / resale | Higher volume, faster to sell | Shallower pool, more variable |

| Vacancy churn | Higher turnover | Lower, longer leases |

| Best suited to | Income-focused investors | End-users and growth-focused buyers |

Common mistakes to avoid

- Chasing yield without counting costs. A headline apartment yield means little until you net off service charges, management fees, and vacancy. Always work with net, not gross.

- Underestimating villa upkeep. Buyers often celebrate the lower community fee, then get surprised by garden, pool, and AC costs. Build a maintenance reserve.

- Assuming community-wide prices. Two units in the same tower or on the same street can differ widely by floor, view, plot, and condition. Never anchor to a district average — value the specific unit.

- Ignoring the tenant pool. A villa in an area with no schools nearby, or an apartment far from transport, fights the very demand it depends on.

- Overlooking supply for apartments. Failing to check the off-plan handover pipeline in your district can leave you competing with a flood of new units at renewal time.

- Forgetting all-in transaction costs. The 4% DLD fee, roughly 2% commission plus VAT, and financing costs are the same rates for both, but far larger in cash on a villa. Budget the total, not just the deposit.

- Buying the asset that suits someone else. An investor buying a family villa for yield, or a family buying a compact apartment for space, is optimising for the wrong outcome.

Conclusion

There is no universally "better" choice between an apartment and a villa in Dubai — only a better choice for a given buyer and goal. Apartments generally offer higher gross yields, lower entry prices, and stronger liquidity, which makes them the natural home for income-focused investors and first-time buyers. Villas generally reward patience with steadier capital growth, deeper end-user demand, and a lifestyle premium, which makes them the natural home for families and long-hold owners who can absorb the higher cost and hands-on upkeep.

Anchor your decision to your own numbers — your deposit, your target return, your appetite for maintenance, and your time horizon — rather than to a headline market figure. If you would like help modelling both options against a specific budget and location, the RERA-certified team at Binayah can run the figures on real, current listings.