UAE real estate Q1 2026: $68.7bn transactions explained

UAE real estate Q1 2026 recorded AED 252.4bn (about $68.7bn) in transactions, marking a robust start to the year across the four leading emirates.

Official reporting picked up a record $68.7bn in transactional value for the first quarter, with Dubai, Abu Dhabi, Sharjah and Ajman all flagged as strong contributors. This snapshot reflects both resale and new-development activity and suggests liquidity and buyer interest remain elevated compared with prior quarters.

For investors the headline matters because it changes relative risk and opportunity. Strong volume tends to support transaction-level pricing and gives lenders and developers scope to adjust product, financing and incentives. This report breaks down what the $68.7bn means for Dubai specifically, how other emirates performed, how market participants are responding, and practical investor actions for the rest of 2026.

What does the Q1 $68.7bn figure mean for Dubai?

What does the Q1 $68.7bn figure mean for Dubai? — Key Data

Q1 Transactions

$68.7bn

Approx AED

AED 252.4bn

Regions

Dubai, Abu Dhabi, Sharjah, Ajman

Source

Arabian Business

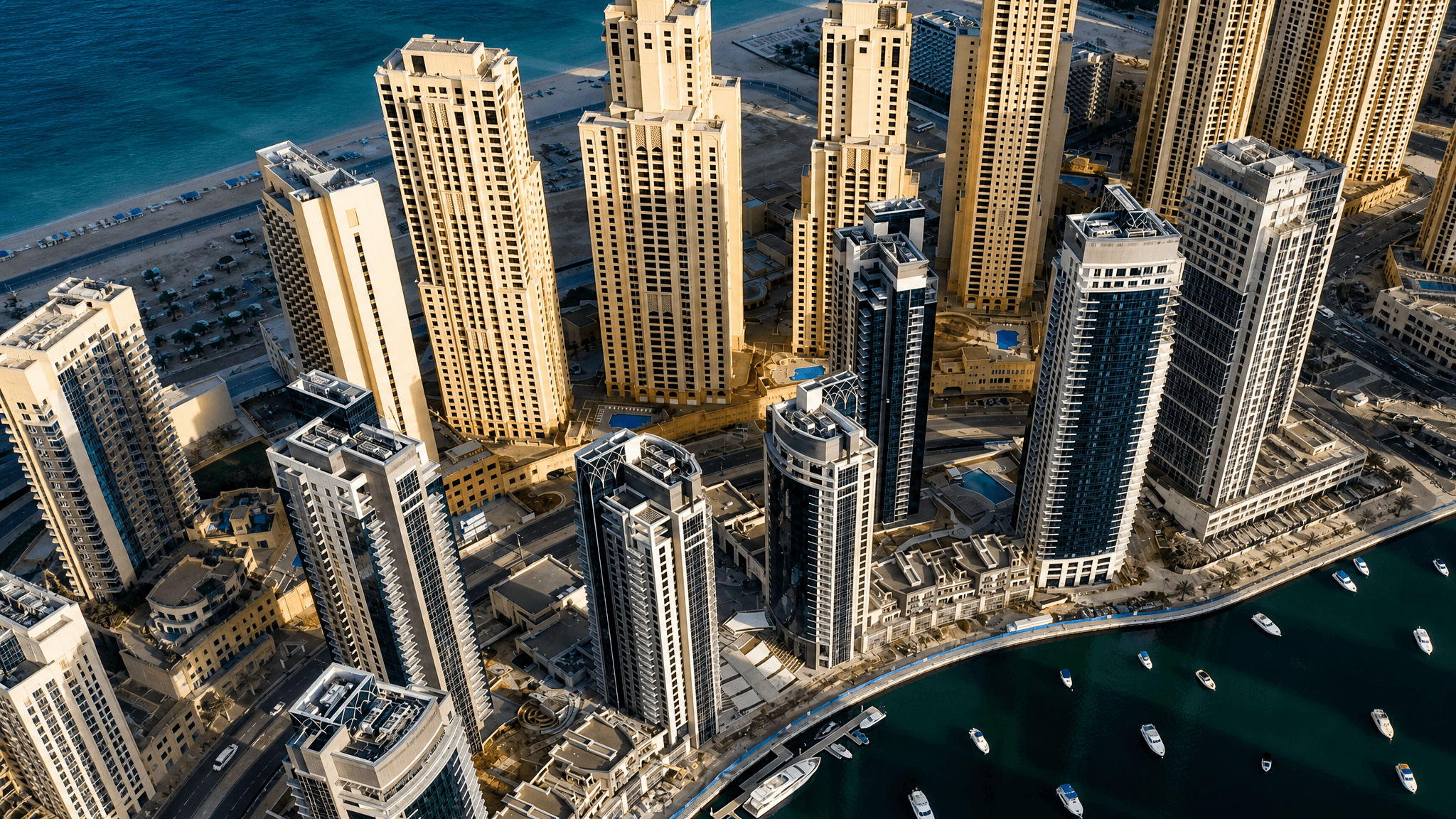

The Q1 $68.7bn headline shows Dubai remained the largest visible driver of UAE real estate activity and sustained demand into 2026. The figure signals a strong start to the year with transactional momentum concentrated in major Dubai corridors and mixed-use hubs.

Dubai's role in producing the headline result is clear because its market still delivers the largest volumes of sales and transfers among the emirates, supporting higher turnover and buyer interest. The $68.7bn total converts to roughly AED 252.4bn using an exchange rate of 1 USD = 3.6725 AED, and that scale gives Dubai more influence over national pricing and sentiment than smaller emirates do.

The nuance for Dubai buyers and sellers is that high transactional value supports liquidity but can also attract speculative flows and price competition. That tends to compress opportunity for bargain purchases while improving exit prospects for short-to-medium term sellers. Investors should therefore prioritise location, developer reputation and yield metrics rather than chasing headline price growth alone.

Which emirates drove the UAE’s Q1 real estate growth?

Abu Dhabi, Sharjah and Ajman all registered strong activity and together reinforced the UAE’s overall $68.7bn Q1 total, showing that the market-wide story is not Dubai-only. Each emirate contributed meaningful transaction volume that helped lift the national figure.

Abu Dhabi's market benefited from targeted demand in urban and suburban segments, while Sharjah and Ajman reported stronger-than-expected transfers in affordable and mid-market stock. The combined activity across these emirates underpinned the $68.7bn total and points to a geographically broader recovery in demand than a Dubai-only headline might suggest.

Investors should recognise that regional dynamics differ: Abu Dhabi pricing and regulatory context vary from Dubai, while Sharjah and Ajman offer different yield profiles and entry prices. Diversifying across emirates can reduce concentration risk but requires understanding local micro-markets and developer track records.

| Emirate | Q1 performance | Notes |

|---|---|---|

| Dubai | Strong transaction volume | Largest contributor to national total |

| Abu Dhabi | Notable urban demand | Different pricing and tenure dynamics |

| Sharjah | Higher mid-market transfers | Affordable segment strength |

| Ajman | Increased resale activity | Value-entry opportunities |

"The $68.7bn Q1 total reflects a multi-emirate recovery rather than a single-city spike; that breadth matters for portfolio allocation decisions."

— Binayah Research Team

How are lenders and developers responding to the Q1 2026 market strength?

How are lenders and developers responding to the Q1 2026 market strength? — Key Data

Q1 Transactions

$68.7bn

Market signal

Increased liquidity

Developer focus

Product and timing

Lender action

Reassessing appetite

Lenders and developers are adjusting strategies in response to the $68.7bn Q1 signal, with banks reassessing appetite and developers calibrating product and launch timing to match demand. The combined market scale gives both groups latitude to refine pricing and incentives.

Banks typically tighten underwriting when volumes spike to control credit risk, or they expand lending where collateral values are firm. Developers often accelerate releases in high-demand corridors and may offer structured payment plans or limited incentives to secure sales while preserving pricing. The $68.7bn headline means more liquidity in the system and more options for buyers and sellers, but it also raises competition for prime stock.

The risk for buyers is faster price repricing and reduced negotiating room in hotspots, while the opportunity is improved exit visibility where liquidity is present. Investors should review lender terms, compare developer escrow and completion records, and stress-test deals against slower sales scenarios despite the strong Q1 numbers.

What should investors do after the Q1 $68.7bn result?

Investors should treat the $68.7bn Q1 result as a sign of sustained market liquidity but not as a guarantee of uninterrupted price growth; position sizing and due diligence become the priority. The headline improves exit visibility yet increases competition in the best locations.

Practical steps include focusing on yield-backed assets in established communities, checking developer delivery records and escrow protections, and comparing financing offers across banks. Given the AED equivalent of roughly AED 252.4bn, the scale of activity supports shorter time-to-sale in liquid locations, but investors must still model downside scenarios and hold periods conservatively.

Risk management matters: diversify by emirate or product type, demand transparent service-charge and rental data, and avoid overpaying for future expectations. Use the Q1 momentum to secure positions with positive cashflow or clear value-add paths rather than speculative leverage on price-only bets.

Key Insight

When transaction volumes spike, liquidity helps exits but compresses bargain opportunities; focus on cashflow, developer completion records and conservative loan-to-value ratios.

- Prioritise yield-positive assets over purely speculative plays

- Check developer escrow and delivery history before committing

- Compare mortgage terms; liquidity can change lending conditions

- Diversify across emirates to reduce concentration risk

The UAE recorded a headline $68.7bn in real estate transactions in Q1 2026, equivalent to roughly AED 252.4bn, with Dubai plus Abu Dhabi, Sharjah and Ajman all contributing. The key takeaway is clear: liquidity is strong, but investors must pair the Q1 momentum with careful due diligence and conservative sizing to manage competition and potential repricing risks.

Binayah Editorial

Property Market Analyst

Our editorial team researches Dubai's real estate market, tracking DLD data, developer launches, and investment trends to keep buyers and investors informed.

Ready to Invest in Dubai?

Speak with our analysts about the best opportunities in today's market — free consultation.