Dubai property market off-plan sales up 9.5% (JLL data)

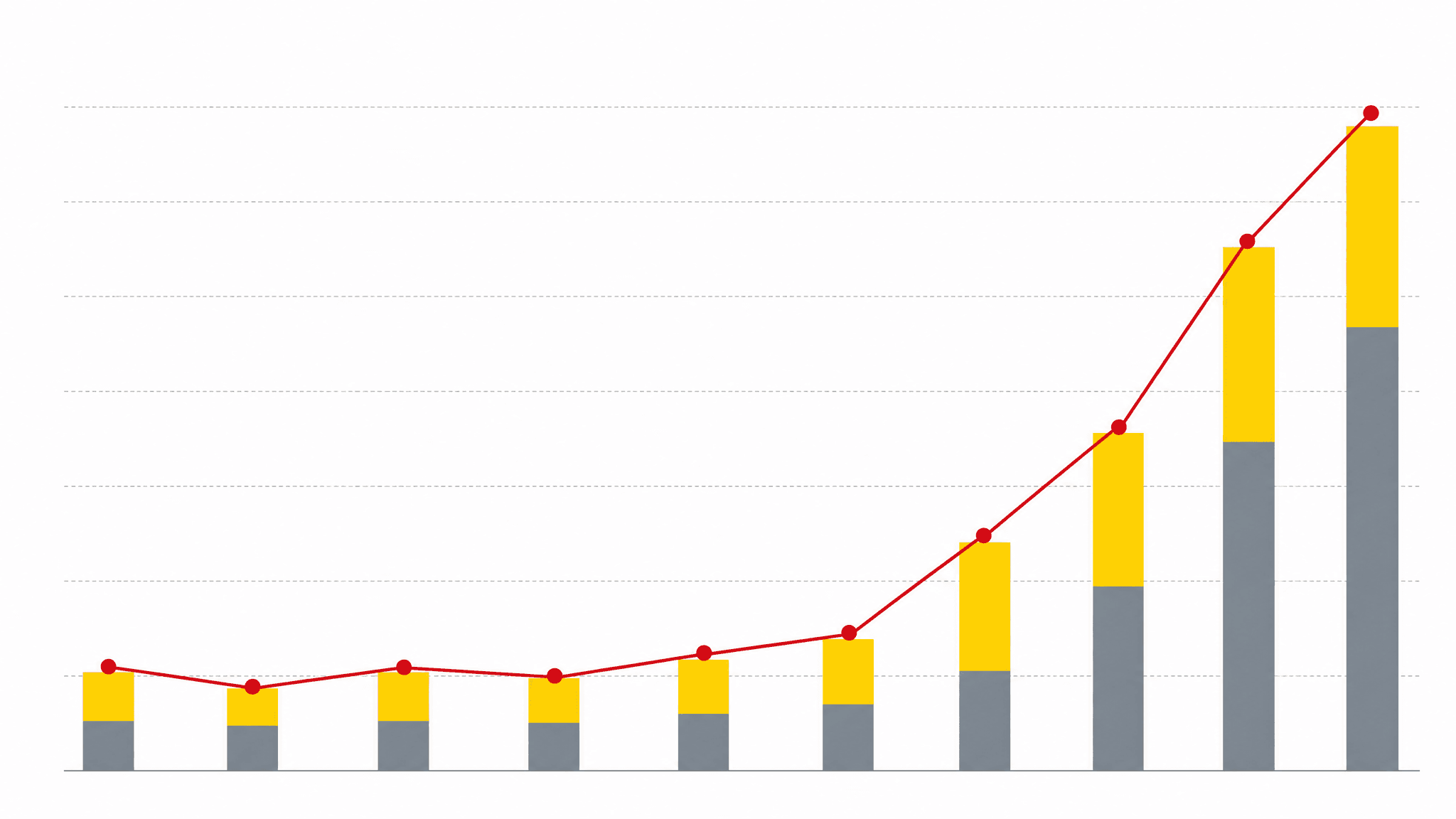

Dubai property market saw off-plan sales gain 9.5% year-on-year while secondary market sales fell 8.2%, according to JLL data in the latest quarter.

The JLL figures show a distinct rotation of demand from resale stock to new development, driven by longer developer payment plans and fresh product specifications. That shift matters for pricing, liquidity and negotiation power: buyers facing lower resale demand have more leverage, while developers can use payment schedules to keep volumes high.

For investors and buyers the immediate implication is tactical: off-plan opportunities are expanding with a clear 9.5% year-on-year uplift, while secondary market vendors may need to adjust expectations after an 8.2% drop. This report breaks down where activity is moving, why off-plan is winning and the practical steps and risks to weigh next.

Where is Dubai property market activity shifting?

Where is Dubai property market activity shifting? Key Data

Off-plan sales

+9.5% y/y

Secondary sales

-8.2% y/y

Source

JLL

Market

Dubai property market

Off-plan activity is growing and capturing a larger share of transactions, with off-plan sales up 9.5% year-on-year while secondary market sales slipped 8.2%, says JLL. This establishes a clear directional shift from resale to new launches in the Dubai property market.

The data shows buyers are choosing new product for reasons developers can influence: extended payment plans, fresh designs and targeted marketing. JLL's 9.5% increase in off-plan sales contrasted with an 8.2% drop in secondary transactions highlights how relatively small percentage moves can change market balance and bargaining power between buyer and seller.

Strategically, this shift changes liquidity patterns and time-to-exit for investors. Sellers in the secondary market may face longer listing times and pricing pressure, while off-plan buyers benefit from staged payments and earlier entry pricing. The durability of the trend will depend on future launch volumes and whether secondary prices stabilise after the 8.2% fall.

Why are off-plan sales rising in Dubai?

Off-plan sales are rising because buyer preference and developer offer align, producing a 9.5% year-on-year increase in off-plan transactions while resale activity fell 8.2%, according to JLL. Payment flexibility and new product are the primary drivers.

Developers have leaned on longer payment schedules and staged handovers to reduce immediate buyer cost, which attracts both end-users and investors to off-plan offers. JLL’s figures make this visible: the 9.5% rise in off-plan sales shows measurable demand capture, while an 8.2% contraction in secondary sales suggests some buyers are re-routing capital into launches rather than resales.

The practical effect is a re-pricing dynamic: launch prices can hold or rise when demand is strong, and secondary sellers confront weaker negotiation positions. Watch product mix closely because peripheral or older resale stock will see disproportionate pressure compared with new, tech-enabled developments.

| Market | Movement | Source |

|---|---|---|

| Off-plan | +9.5% y/y | JLL |

| Secondary | -8.2% y/y | JLL |

"The 9.5% uplift in off-plan sales shows developers are successfully converting interest through payment plans and product refresh; resale markets are adjusting price expectations accordingly."

— Binayah Research Team

What is the investment outlook and practical steps for investors?

Investors should prioritise off-plan opportunities while monitoring secondary market pricing, because off-plan sales rose 9.5% y/y and secondary sales fell 8.2% y/y, per JLL. That mix creates buying windows in both segments depending on strategy and risk appetite.

Practically, start by comparing developer payment terms and handover timelines; longer payment plans can reduce cash drag and improve effective entry pricing versus immediate purchase on the secondary market. Use the JLL split as a signal: higher off-plan demand implies potential capital gain on launch pricing, while the 8.2% fall in secondary sales suggests negotiation room for cash buyers in resale.

For risk management, stress-test exit scenarios and consider liquidity: off-plan holdings require longer capital lock-up and depend on developer completion, while secondary assets can be more liquid but face price compression. Track JLL updates and transaction-level data to time entries and exits around 9.5% and 8.2% market moves.

- Compare payment plans and completion dates

- Verify escrow and developer track record

- Model cashflow versus secondary price discounts

- Monitor JLL data for market direction

What risks should Dubai property buyers watch next?

The immediate risk is a secondary market price correction as resale sales fell 8.2% year-on-year while off-plan rose 9.5%, according to JLL. That divergence can pressure resale values and create short-term liquidity mismatches for sellers.

Other risks include developer delivery schedules, which can extend investor holding periods, and concentrated supply in certain communities that could blunt price recovery. The JLL figures do not specify which submarkets moved most, so buyers and investors should treat the 9.5% off-plan increase and 8.2% secondary decline as broad signals, then layer community-level checks before committing capital.

Watch for three leading indicators: new launch absorption rates, resale days on market and announced delivery delays. These will tell whether off-plan momentum is structural or a shorter rotation caused by tactical incentives from developers.

Key Insight

Investors should not assume off-plan demand eliminates secondary market risk. The 8.2% fall in resale sales indicates price pressure; always verify developer completion history and run worst-case cashflow scenarios before committing.

The JLL snapshot shows a clear rotation: off-plan sales rose 9.5% year-on-year while secondary market sales fell 8.2%, shifting bargaining power and liquidity patterns in the Dubai property market. Investors and buyers should use those percentage signals to prioritise due diligence, compare payment plans and track resale absorption at the community level before acting.

Binayah Editorial

محلل سوق العقارات

يبحث فريق تحريرنا في سوق العقارات في دبي، ويتتبع بيانات DLD وإطلاق المشاريع والاتجاهات الاستثمارية.

هل أنت مستعد للاستثمار في دبي؟

تحدث مع محللينا حول أفضل الفرص في السوق اليوم — استشارة مجانية.